Oops! Something went wrong while submitting the form.

Stablecoins proved that financial value could move globally through public blockchain networks. Nearly $300 billion now circulates onchain, creating financial infrastructure that operates across borders, wallets, exchanges and applications.

Tokenized Treasuries, funds and other financial instruments followed. More than $27 billion in distributed real-world asset value is now tracked onchain, including over $10 billion in tokenized U.S. Treasuries.

This growth matters. It also represents a small fraction of global securities markets.

The next phase will be determined by what happens after an asset is tokenized.

Can it move across approved markets? Can ownership be updated without reconciling several disconnected records? Can investors reuse verified credentials? Can the asset enter custody, secondary markets, credit and collateral applications while preserving the controls attached to it?

Creating the token is the first step. The market infrastructure around it determines what the asset can do next.

Securities markets depend on authoritative records.

The issuer needs to know who owns the asset. The transfer agent needs to maintain the official investor registry. Eligibility conditions, transfer restrictions, servicing actions and issuer controls need to remain tied to the same record throughout the asset’s lifecycle.

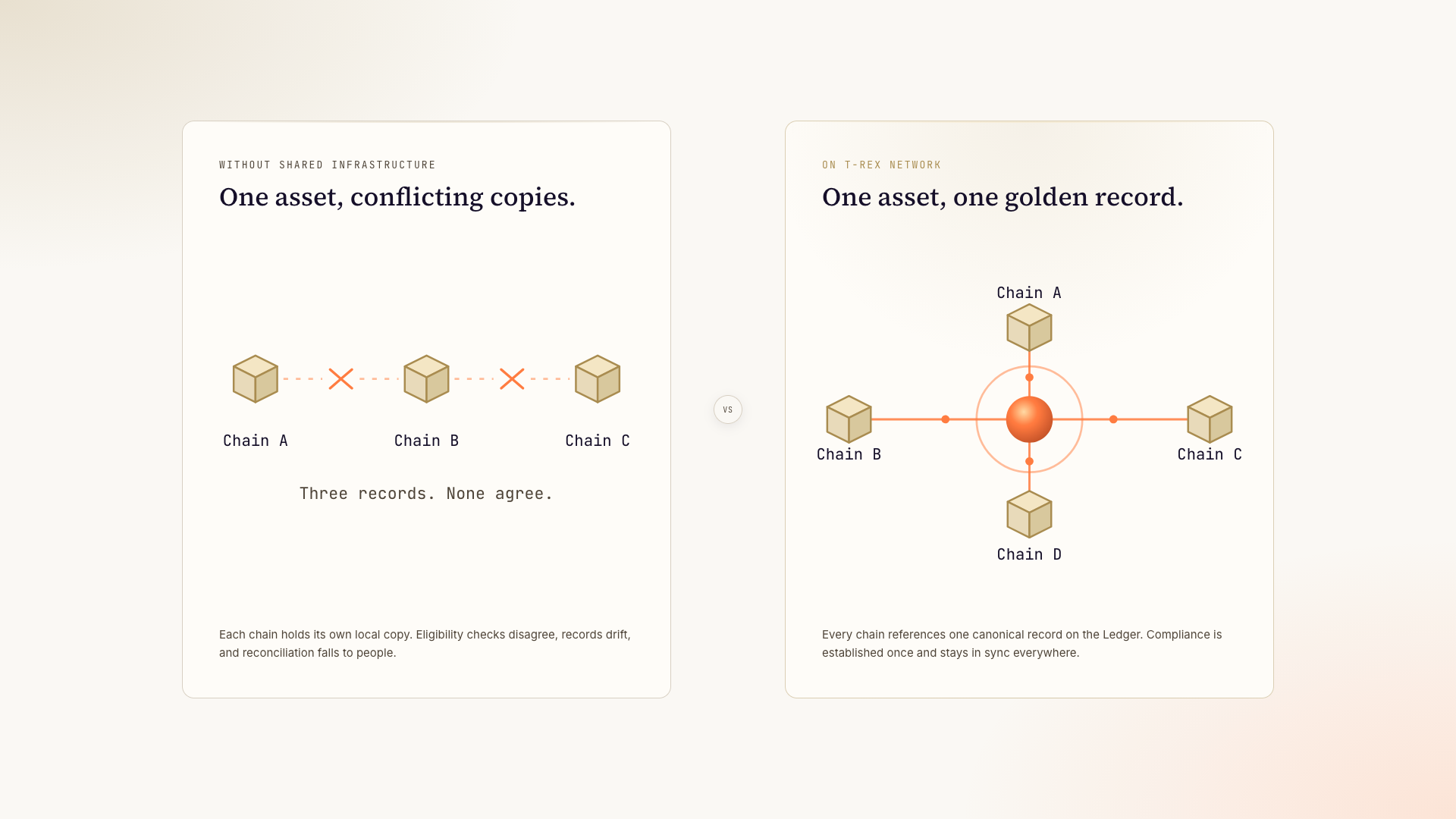

Many tokenized securities still operate as digital twins of an offchain register. The token represents the security onchain, while the authoritative record of ownership remains in another system.

That creates another representation to reconcile.

A transfer recorded onchain may still need to be reflected in an offchain register. Ownership changes need to remain consistent between both systems. Freezes, redemptions, recoveries and corporate actions need to be coordinated across separate records.

The token may improve parts of the workflow. The underlying market still depends on the original book of record.

Moving that book onchain changes the foundation.

The primary registry is the authoritative record of who owns the security and under which conditions that ownership can change.

Bringing it onchain makes the register programmable.

Ownership, investor identity, eligibility, compliance rules and issuer controls can operate through the same infrastructure used to transfer and service the asset. Approved venues, blockchains, counterparties and applications can interact with the authoritative record instead of maintaining disconnected versions of it.

This changes what tokenization can support after issuance:

These outcomes do not come from the token alone. They depend on the record, rules and market participants surrounding it.

“Turning the token from something you hold into something you can fund, lend against, and settle with. Issuance gets almost all the attention ("we put the asset on-chain"), and everyone quietly assumes utility follows. It doesn't. A tokenized bond or fund interest with no venue, no repo, no credit line, no margining is just a digital certificate sitting idle — which is exactly why the vast majority of tokenized RWAs trade with near-zero secondary volume. A tokenized-collateral rail is necessary but not sufficient; the market that puts the collateral to work is the underbuilt part,” said Dennis O'Connell, CEO of Ascend.

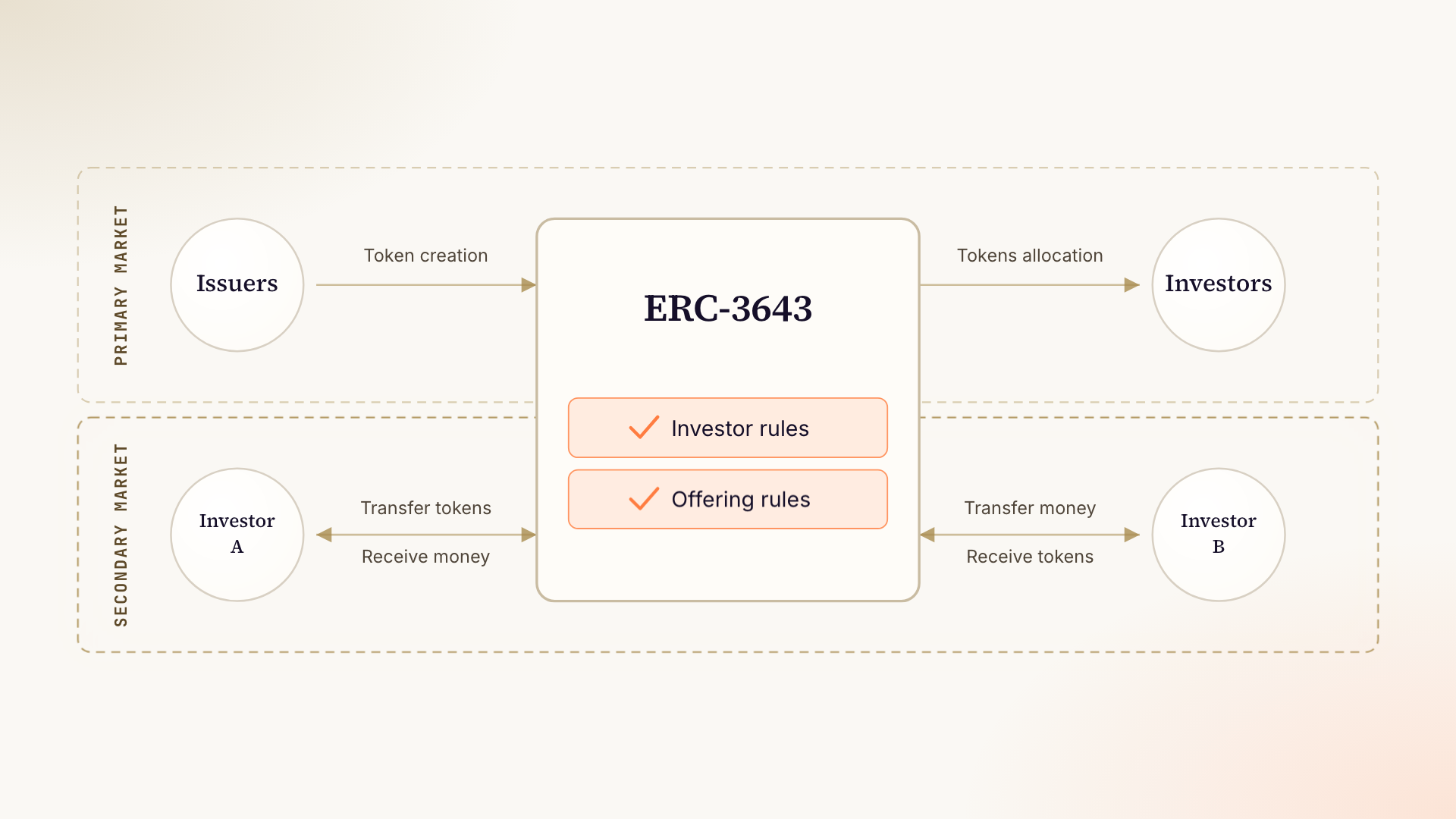

ERC-3643 began as the T-REX Protocol, created and open-sourced by Tokeny. It extends ERC-20 with the identity, compliance and lifecycle controls required for regulated financial instruments.

An investor’s wallet can be linked to an ONCHAINID containing verified claims from approved third parties. Before ownership changes, the asset can check whether the investor holds the required credentials, whether those credentials came from a trusted issuer and whether the transfer satisfies the active rules.

The standard also supports recovery, freezing, forced transfers, minting and burning, giving issuers and their appointed agents the controls required after issuance.

ERC-3643 association members have supported more than $32 billion in cumulative tokenized asset value using the standard across multiple jurisdictions.

ERC-3643 established how ownership and compliance controls can operate through the asset. T-REX moves the wider securities registry onchain.

T-REX brings ownership, identity, eligibility, compliance and issuer controls into one authoritative book of record.

The token no longer needs to function as a mirror of a register maintained elsewhere. The register itself becomes programmable infrastructure for tokenized securities markets.

That registry also needs to work across chains.

Issuers will use different networks to reach different investors, venues and applications. Market structure will remain fragmented if each environment creates its own ownership record, investor registry and compliance state.

T-REX Ledger provides the shared reference across approved networks.

Our dedicated Layer 2 is built using Polygon CDK and connected to participating networks through Agglayer. Each network retains its own settlement infrastructure while working from the same current ownership and compliance record.

Apex Group, which services more than $3.5 trillion in assets, will act as the onchain transfer agent at launch. Apex has adopted T-REX Ledger as its default multi-chain infrastructure and announced a target of $100 billion in tokenized assets by June 2027.

"Settlement can stay distributed — that's fine. What can't be distributed is the truth. When a tokenized security lives across multiple chains, venues and applications, each environment needs to reference a single authoritative record of ownership, identity and compliance state. Otherwise you get five venues with five versions of who owns what and who's allowed to trade it. Shared record, distributed execution — that's the market structure that scales," said Michael Steuer, the CTO of the Casper Association, who are building a native implementation of ERC-3643 and integration with the T-REX Network on the Casper blockchain

A tokenized security becomes useful when it can move, settle, be serviced, support collateral and connect with financial applications while preserving valid ownership and enforceable controls.

That requires more than a digital representation.

It requires an authoritative book of record that approved market participants can build around.

ERC-3643 provides the open token standard. ONCHAINID connects verified investors with their wallets and credentials. T-REX Ledger coordinates the ownership record and controls across connected networks. The T-REX AppStore connects those assets with compatible financial applications.

Together, this infrastructure turns the securities register into a foundation for market activity.

That is how tokenization moves from digital representation to capital markets infrastructure, and how tokenized securities begin to support real distribution, settlement, servicing and financial utility after issuance.

Bringing the next trillion USD of assets onchain, thanks to a proven compliance framework and the largest interoperable ecosystem.